Which is the correct order of steps in the accounting cycle?

Jul 01, 2021 · Steps one through seven occur every accounting period—regardless of length—while step eight only occurs at the end of the fiscal year: 1. Analyze transactions. The first step in the accounting cycle is to analyze events to determine if …

What are the 10 steps of accounting cycle?

Jul 23, 2021 · The accounting cycle is a term that describes the bookkeeping process in which you maintain detailed records of your business’ or account’s credits and debits. Accounting Cycle: 9 Steps of the Accounting Cycle Process - 2022 - MasterClass

What are the six steps in the accounting cycle?

Jun 16, 2020 · The Nine steps in the Accounting Cycle are as follows: Step 1: Analyze Business Transaction. Step 2: Journalize Transaction. Step 3: Posting To Ledger Account. Step 4: Preparing Trial Balance. Step 5: Journalize & Post Adjustments. Step 6: Prepare Adjusted Trial Balance. Step 7: Prepare Financial Statements.

What are the steps in accounting cycle?

Dec 24, 2019 · Thus, Accounting Cycle includes: entering transaction; processing, classifying and adjusting the business transactions through the accounting cycle; closing books of accounts at the end of an accounting period and; starting the cycle again for the next accounting period; Accordingly, an accounting cycle has the following nine basic steps.

What is the correct order of steps in the accounting cycle quizlet?

Which is the correct order of steps in the accounting cycle? Journalize and post transactions, journalize and post adjusting entries, journalize and post closing entries.

What is the correct order of sixth steps of the accounting cycle?

We will examine the steps involved in the accounting cycle, which are: (1) identifying transactions, (2) recording transactions, (3) posting journal entries to the general ledger, (4) creating an unadjusted trial balance, (5) preparing adjusting entries, (6) creating an adjusted trial balance, (7) preparing financial ...

What are the 5 steps of the accounting cycle?

Defining the accounting cycle with steps: (1) Financial transactions, (2)Journal entries, (3) Posting to the Ledger, (4) Trial Balance Period, and (5) Reporting Period with Financial Reporting and Auditing.

What are the 4 steps of the accounting cycle?

First Four Steps in the Accounting Cycle. The first four steps in the accounting cycle are (1) identify and analyze transactions, (2) record transactions to a journal, (3) post journal information to a ledger, and (4) prepare an unadjusted trial balance. We begin by introducing the steps and their related documentation ...Apr 11, 2019

What are the 6 process of accounting?

The steps of the accounting process are analyzing, recording, classifying, summarizing, reporting, and interpreting. Computers are often used in the recording, classifying, summarizing, and reporting.

What are the 10 steps of accounting cycle?

10 Steps of the Accounting CycleAnalyzing transactions.Entering journal entries of the transactions.Transferring journal entries to the general ledger.Crafting unadjusted trial balance.Adjusting entries in the trial balance.Preparing an adjusted trial balance.Processing financial statements.Closing temporary accounts.More items...

What are the 3 steps in the accounting process?

Part of this process includes the three stages of accounting: collection, processing and reporting.

What are the 10 steps in the accounting cycle PDF?

10 Steps of Accounting Cycle [Notes with PDF]Identification of Transaction.Journalizing.Posting to Ledger.Preparation of Trial Balance.Adjusting Entry.Adjusted Trial Balance.Preparation of Financial Statement.Closing Entry.More items...

How many steps are there in the accounting cycle?

The accounting cycle consists of eight steps that accountants should follow to record transactions and check for data accuracy. Steps one through seven occur every accounting period—regardless of length—while step eight only occurs at the end of the fiscal year:

What is the accounting cycle?

The accounting cycle is a series of steps used by an accounting department to document and report a company's financial transactions. The cycle follows financial transactions from when they occur to how they affect financial documents. The accounting cycle happens every accounting period or reporting period for which financial documents are ...

When is the next fiscal year?

For example, the government uses a fiscal year of October 1 to September 30. For the government, Fiscal Year 21 (usually denoted as FY21) runs from October 1, 2020 to September 30, 2021. If the government uses monthly accounting periods, then Period 1 of FY21 would be October 2020. Period 4 of FY21 would be January 2021.

What is a general ledger account?

Post entries to the general ledger. A ledger account is a collection of all journal entries that debit or credit that account. The general ledger is the master set of all ledger accounts. The general ledger keeps track of a company's entire financial activity.

What is an unadjusted trial balance?

At the end of each accounting period, a company's accounting department should enter the data from the ledger accounts into a trial balance. This trial balance is also called “the unadjusted trial balance” because it is prepared before adjusted entries—step six—being entered.

Do publicly traded companies have to file quarterly financial statements?

For example, the SEC requires publicly traded companies to file financial statements quarterly, so these companies will have quarterly accounting periods to meet this requirement. Companies must also file yearly tax forms with the IRS, so these companies will have yearly accounting periods to meet this requirement.

What Is the Accounting Cycle?

The accounting cycle is a bookkeeping process by which small businesses and large corporations alike take each individual credit and debit balance they accrue and transform them into an overall financial statement. Putting these accounting principles into practice helps appraise a company’s financial activities and render them intelligible overall.

The Importance of Accurate Bookkeeping for Financial Statements

Accurate bookkeeping is an essential practice for assessing the health of your business, both internally and externally. The financial statements created toward the end of the accounting cycle can help you measure the viability and durability of your business’s financial wellness in every arena.

9 Steps of the Accounting Cycle Process

The accounting cycle is the cornerstone of many managed accounting systems. Here are the nine steps in the accounting cycle process:

What is the accounting cycle?

The accounting cycle is a process designed to make financial accounting of business activities easier for business owners. There are usually eight steps to follow in an accounting cycle. The closing of the accounting cycle provides business owners with comprehensive financial performance reporting that is used to analyze the business.

What is the second step in the cycle?

The second step in the cycle is the creation of journal entries for each transaction. Point of sale technology can help to combine steps one and two, but companies must also track their expenses. The choice between accrual and cash accounting will dictate when transactions are officially recorded. Keep in mind, accrual accounting requires the matching of revenues with expenses so both must be booked at the time of sale.

Why do companies use accounting software?

Many companies use accounting software to automate the accounting cycle. This allows accountants to program cycle dates and receive automated reports. Depending on each company’s system, more or less technical automation may be utilized.

When is cash accounting recorded?

Cash accounting requires transactions to be recorded when cash is either received or paid. Double-entry bookkeeping calls for recording two entries with each transaction in order to manage a thoroughly developed balance sheet along with an income statement and cash flow statement.

Why is recordkeeping important?

Each one needs to be properly recorded on the company’s books. Recordkeeping is essential for recording all types of transactions. Many companies will use point of sale technology linked with their books to record sales transactions. Beyond sales, there are also expenses that can come in many varieties.

What is double entry accounting?

Double-entry accounting is required for companies to build out all three major financial statements: the income statement, balance sheet, and cash flow statement.

What is a general ledger?

Once a transaction is recorded as a journal entry, it should post to an account in the general ledger. The general ledger provides a breakdown of all accounting activities by account. This allows a bookkeeper to monitor financial positions and statuses by account.

What is accounting cycle?

Accounting cycle is a process of a complete sequence of accounting procedures in appropriate order during each accounting period. Accounting process is a combination of a series of activities that begin when a transaction takes place and ends with its inclusion in the financial statements at the end of the accounting period. ...

What is the financial statement prepared from?

Financial statements are prepared from the balances from the adjusted trial balance. The financial statements are made at the very last of the accounting period. Cash flow statement, income statement, balance sheet and statement of retained earnings; are the financial statements that are prepared at the end of the accounting period.

How to make sure that debits equal credits?

To make sure that debits equal credits, the final trial balance is prepared . As the temporary ones have been closed only the permanent accounts appear on the closing trial balance to make sure that debits equal credits.

What is a general journal?

Journalizing the transaction. Transactions having an impact on the financial position of a business are recorded in the general journal. In the general journal, the transactions are recorded as a debit and a credit in monetary terms with the date and short description of the cause of the particular economic event.

What is an unadjusted ledger?

It is a way to investigate and find the fault or prove the correctness of the previous steps before proceeding to the next step.

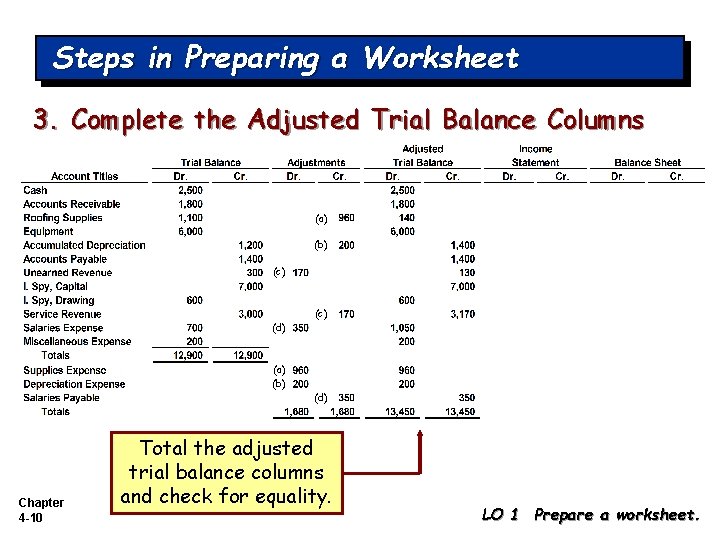

What is an adjusted trial balance?

An adjusted trial balance contains all the account titles and balances of the general ledger which is created after the adjusting entries for an accounting period have been posted to the accounts.

What is a Posit closing entry?

Posit closing entries is an optional step of the accounting cycle. A reversing journal entry is recorded on the first day of the new period for avoiding double counting the amount when the transaction occurs in the next period.