How do you make a statement of cash flow?

- Operating activities cash flow. This is the money your business generates and spends on typical, day-to-day operating activities, such as selling products and services or paying rent and employees. ...

- Investing activities cash flow. ...

- Financing activities cash flow. ...

What is UCA cash flow analysis?

UCA cash flow or Uniform Credit Analysis cash flow, is one method used to determine the ability of a company to repay a loan.

What does the cash flow statement tell you?

Three Sections of a Statement of Cash Flows are:

- Cash from operating activities,

- Cash from investing activities,

- Cash from financing activities.

How are cash flows classified in a cash flow statement?

Set 10: Cash Flows

- The Statement of Cash Flows:

- The purchase of land is classified in the statement of cash flows as a(n):

- The issuance of notes payable for borrowing is classified in the statement of cash flows as:

- The purchase of treasury stock is classified in the statement of cash flows as a(n):

- Operating cash flows exclude:

What is UCA cash flow?

What is UCA cash flow analysis?

What is the purpose of accountant for UCA?

How is UCA cash flow calculated?

A: The basic UCA Cash Flow calculation consists of adjusting each income statement line item by adding or subtracting the net change in each balance sheet counterpart account.

Is UCA cash flow direct or indirect?

direct cash flowA: The UCA cash flow statement, as presented it in the webcast, is an example of the direct cash flow methodology. Direct cash flow follows the sequence of the income statement and modifies each component in the income statement by the net change of counterpart balance sheet accounts.

What is a difference between the UCA cash flow model and the traditional cash flow model?

Which option identifies an advantage of the UCA model over a traditional statement of cash flows? The UCA model provides more information about the cash flow impact of sales, gross margin, and operating expenses.

Is EBITDA a cash flow?

Key Differences Operating cash flow tracks the cash flow generated by a business' operations, ignoring cash flow from investing or financing activities. EBITDA is much the same, except it doesn't factor in interest or taxes (both of which are factored into operating cash flow given they are cash expenses).

What is difference between direct and indirect cash flow?

The indirect method uses net income as the base and converts the income into the cash flow through the use of adjustments. The direct method only takes the cash transactions into account and produces the cash flow from operations.

What is cash EBITDA?

Cash EBITDA is a measure of actual performance from the collection business (cash business) and other business areas. EBITDA. Earnings before interest, taxes, depreciation, and amortization. Factoring.

What is traditional cash flow?

Traditional Cash Flow means net income after taxes and dividends, plus depreciation, amortization and other non-cash charges. Traditional Cash Flow means net income after taxes, plus depreciation, amortization and other non-cash charges.

How do you calculate surplus in finance?

Surplus is the amount of an asset or resource that exceeds the portion that is utilized. To calculate consumer surplus one merely needs to subtract the actual price the consumer paid by the amount they were willing to pay.

What is cash flow coverage ratio?

The cash flow coverage ratio is a liquidity ratio that measures a company's ability to pay off its obligations with its operating cash flows. In other words, this calculation shows how easily a firm's cash flow from operations can pay off its debt or current expenses.

Why is EBITDA not cash flow?

EBITDA does not account for changes in working capital (current assets minus current liabilities) and the cash required to run the daily operating activities. Ignoring working capital requirements assumes that a business gets paid before it sells its products.Nov 13, 2011

Is EBITDA good proxy for cash flow?

The Earnings Before Interest Taxes Depreciation and Amortization (or EBITDA) is a measure of the operating profitability of a company. The EBITDA has 2 main advantages: it is very easy to compute and it is a good proxy of the company's operating cash flow.

Is EBITDA same as free cash flow?

Key Takeaways Free cash flow (FCF) and earnings before interest, tax, depreciation, and amortization (EBITDA) are two different ways of looking at the earnings generated by a business. EBITDA sometimes serves as a better measure for the purposes of comparing the performance of different companies.

What is UCA cash flow? - AskingLot.com

Click to see full answer. Thereof, what is a UCA cash flow statement intended to focus on? The Uniform Credit Analysis, or UCA Cash Flow, is designed to help you identify where the business's cash is going and how it is being used. Is it being used to purchase additional inventory or is it being used to purchase equipment?

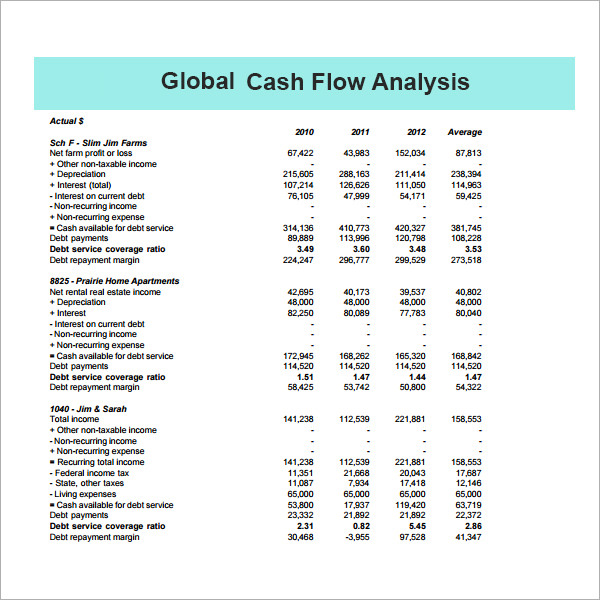

Cash Flow Analysis Modified UCA Cash Flow Format

C. Mulford: Cash Flow Analysis, p. 2 Income Statement Statement Data Cases 1 - 3 Amounts in (000's) Sales $ 8,000 Cost of Goods Sold (incl. dep'n of $800) $ 4,960

Cash Flow Analysis I: UCA Fundamentals Course | RMA

Course Overview. RMA’s Cash Flow Analysis I: UCA Fundamentals teaches the fundamentals of constructing and analyzing direct and indirect cash flow statements so that a credit analyst will have clearer insights into how a company generates and uses its cash resources.

Cash Flow Analysis - RMA U

ent Cash EBITDA (which we could call CEBITDA). In this case, CEBITDA was a positive $758,000 to cover the $284,000 in interest for a coverage ratio of 2.6.

ABA Agricultural Bankers Conference 2021

The FINPACK team at ABA Agricultural Bankers Conference The FINPACK team was pleased as always to participate in the 2021 ABA Agricultural Bankers Conference in Cincinnati. We were proud to host the Pre-Conference Seminar together with Farmer Mac, featuring...

2021 ABA National Agricultural Banker Conference

Make plans to join the FINPACK Team in Cincinnati at the 2021 ABA National Agricultural Bankers Conference Nov. 14-17. FINPACK, Farmer Mac, and Dr. Kohl kick off the conference on Sunday afternoon as hosts of the Pre-Conference Seminar titled, "Speeding...

Register for the 2021 FINPACK Lenders Conference

After much thought and discussion, the decision has been made to change the 2021 FINPACK Lenders Conference to a virtual-only event. Our goal is a safe event for all attendees. 2021 Conference Details Date: December 14-15, 2021 Location: Virtual Pre-registration is...

CALCULATING CASH PAID TO SUPPLIERS

This is pretty much self explanatory. If you are a shoe retailer, you would deduct the price that you pay for the shoes to the manufacturer

CALCULATING CASH PAID FOR OPERATING COSTS

Operating costs is another easy one. In this particular section you deduct all of your operating expenses such as wages, rent, insurance, taxes etc. At the same time you will account for those expenses that have not resulted into an actual cash outflow, but have instead created an accrual.

THE RESULT IS YOUR NET CASH FLOW FROM OPERATIONS (NCAO)

The resulting number after accounting for the above will be the NCAO, If your lender uses this type of cash flow calculation he will take this number and divide it by the amount of debt service that your loan request needs to come up with a ratio.

CALCULATING CASH PAID TO SUPPLIERS

This is pretty much self explanatory. If you are a shoe retailer, you would deduct the price that you pay for the shoes to the manufacturer

CALCULATING CASH PAID FOR OPERATING COSTS

Operating costs is another easy one. In this particular section you deduct all of your operating expenses such as wages, rent, insurance, taxes etc. At the same time you will account for those expenses that have not resulted into an actual cash outflow, but have instead created an accrual.

THE RESULT IS YOUR NET CASH FLOW FROM OPERATIONS (NCAO)

The resulting number after accounting for the above will be the NCAO, If your lender uses this type of cash flow calculation he will take this number and divide it by the amount of debt service that your loan request needs to come up with a ratio.

Does unrealized loss affect cash flow?

Since the loss is unrealized, obviously there is no affect on cash flow. The investment would be written down by the amount of the unrealized loss (decrease in asset is a source of cash) and the loss would be expensed on the income statement (use of cash). You can spread that one of two ways. The preferred way would be to write the asset up to the initial investment amount and not show the non-cash expense in the operating cash flows. The other (which I do not recommend) would be to use the current value of the asset and spread the loss as an expense in the operating cash flows section. Either way, total cash flow is not affected. However, in the latter way, business cash income would be understated because the expense is captured in the operating cash flows that sum to business cash income and the investment itself is spread with investing activities in the same part of the cash flow statement as fixed asset and intangible asset spending. I encourage you to spread it the first way because business cash income is a key indicator in risk assessment and so we want to get that number right.

Do UCA statements have to be accrual based?

Q: Must the income statement used in constructing a UCA cash flow statement be accrual-based?#N#A: The income statement used in building a UCA cash flow statement does not have to be accrual based, but it is rare for a company to keep an income statement on a cash basis. Those that do so are usually small businesses that accept only cash for the services they provide and pay all expenses in cash only.#N#The vast majority of companies use the accrual method of accounting to record sales as they meet all the Generally Accepted Accounting Principles (GAAP) criteria to cause statements to fairly and accurately depict all business activity for the period measured. Generally GAAP also call on a business to apply the Matching Principle in recognizing production costs and operating expenses. GAAP causes the business to present sales and costs on the income statement in this way regardless of whether cash has exchanged hands in completing a sale or recognizing costs.#N#Note that the IRS will allow companies to report income on a cash basis if, in general, their sales are less than $5 million. Note also that other severe restrictions apply in doing so. Almost invariably, the companies in question keep their books on an accrual basis, using a cash basis for income tax reporting because it may result in less tax.#N#All publicly traded companies must use accrual accounting.#N#Q: If we were to make a credit offer to Tampa Bay Leisure, how could we prevent the continued use of short-term debt to fund long-term assets?#N#A: An important first step might be to offer long term financing to more properly restructure the company’s borrowing and eliminate the misuse of short term borrowing, most likely the company’s line of credit. Doing so frees up the misused portion of their short term borrowing capacity and reset their cash flows.#N#Restructuring a company’s borrowing also sets the stage for conversation to establish more discipline around future use of a line of credit or other short term borrowing. Establishing a tight borrowing base requirement can effectively set the stage for more carefully monitored draws and provide assurance that the line of credit draws are indeed made to support only eligible inventory and receivables. To be most effective, the lender should manage the frequency of a borrower’s submission of the borrowing base to better assure current information as well as assure that the line is meeting current requirements. Another useful discipline is to ask for or generate projections based on management input to identify, as closely as possible, forthcoming borrowing causes and needs. If no short-term borrowing causes, reduce the short term line or amount available accordingly.

What is UCA cash flow?

UCA cash flow or Uniform Credit Analysis cash flow , is one method used to determine the ability of a company to repay a loan. Some would say UCA cash flow analysis is a more accurate, practical and easily understandable method to determine this ability, versus methods such as EBITDA (earnings before interest, taxes, depreciation and amortization), or net income plus depreciation. We provide a simplified definition of UCA cash flow.

What is UCA cash flow analysis?

UCA cash flow analysis eliminates issues such as non-cash expenses for equipment depreciation, or inflated cash flow based on extending the time to pay vendors.

What is the purpose of accountant for UCA?

An accountant can help you further understand the definition of UCA cash flow, how it applies to your situation, and help you put a UCA cash flow analysis together. If you don’t already have an accountant that you trust, you should use TalkLocal to find an accountant.