- Positive Accounting. Positive economic theory and accounting practices are objective and based on fact. ...

- Normative Accounting. Normative economic theory is subjective and aims to describe what the economic future should be for a company or investor.

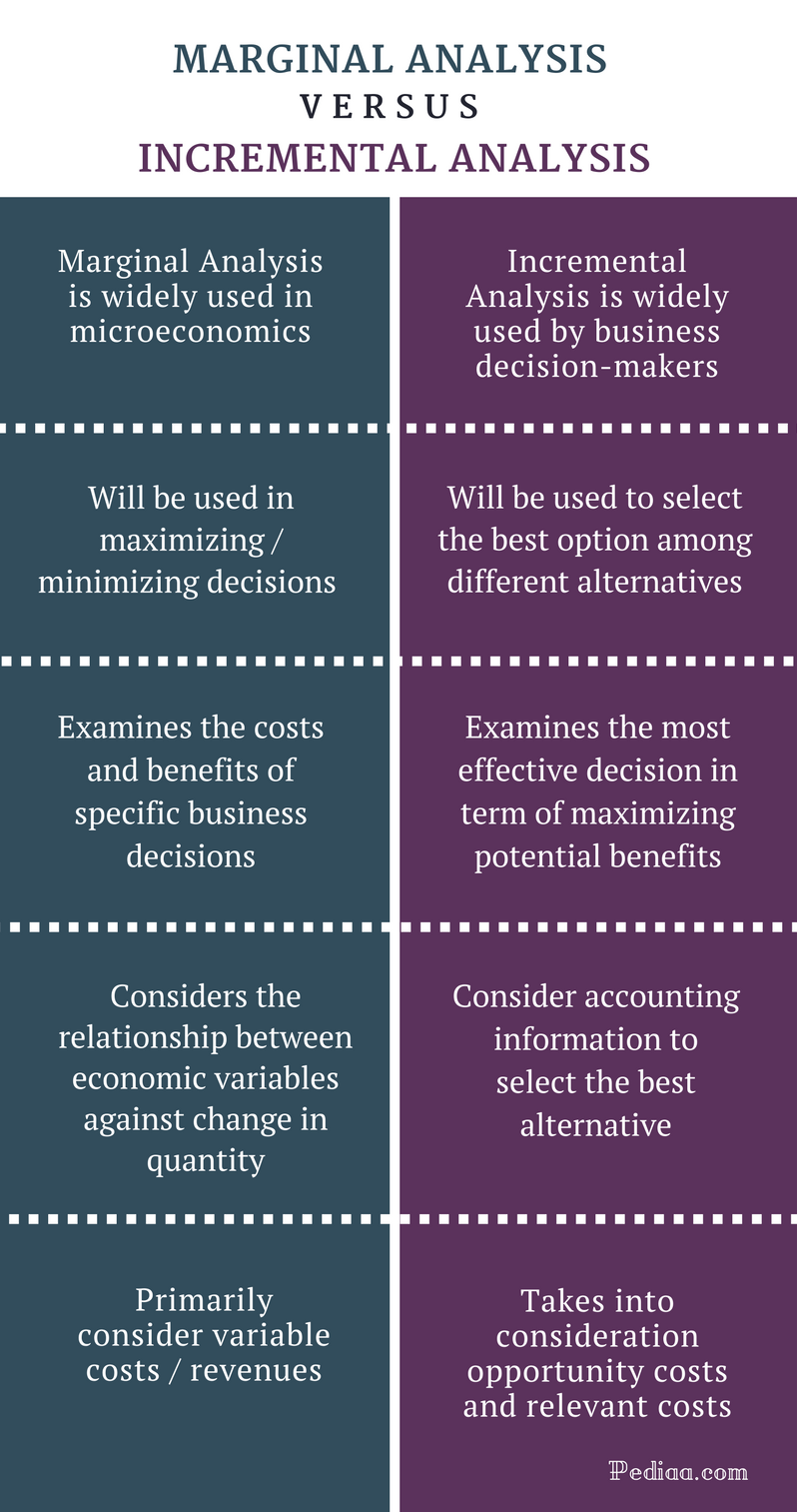

- When to Use. ...

- Working Together. ...

How do normative and positive accounting theories complement each other?

In this way, the two theories complement each other, each filling in for the weaknesses of the other. Positive accounting is very practical, and based on what's actually happening. Normative is more theoretical, ensuring that, as day-to-day practices evolve, they don't diverge from appropriate economic concepts.

What is the positive theory of accounting?

Executive Summary: Positive theory of accounting explains many concepts that assist us clarify and anticipate the various accounting methods that firms and businesses have pursued. They tend to consider the occurrences taking place in society and incorporate them into accounting practices as per their translations.

Is the normative principle of accounting still relevant?

Although, normative principle of accounting has its upsides, in some ways the same has been condemned. The normative principle of accounting is focused on some or the other assessment of quality which makes the situation a little different. Furthermore, there is no quantitative hypothesis testing in the normative accounting theory.

What is the normative accounting model?

In the normative accounting model, the analysts appear to stick to a few different philosophies which they find and, depending on the same methodology, attempt to reach any conclusion that can be guided to achieve a possible solution. The normative theory can help shape both the consumer and the firm's economic outlook.

What is a normative accounting theory?

Normative Accounting Theory is an explanation or reasoning to justify the feasibility of an accounting treatment that is most in line with the stated objectives. Better explain accounting practices that should apply (it should be) and value is used as the main target.

What are the differences between normative and positive researches in the context of accountancy business research?

Researchers perform two main types of research, positive and normative. Positive research is the branch of academic research in accounting that seeks to explain and predict actual accounting practices. Normative research, in contrast, seeks to derive and prescribe "optimal" accounting standards.

What is the meaning of positive accounting theory?

Positive accounting theory seeks to explain a process, which uses the ability, understanding and knowledge of accounting and the use of accounting policies that are most suitable for dealing with certain conditions in the future.

What are the two different types of theories in accounting?

Two of the most common and influential theories are positive accounting and normative accounting.

What is an example of positive theory?

In economics, positive theories attempt to explain how the economy actually operates and include, for example, the basic supply and demand models of microeconomics as well as the macroeconomic theories of Keynesian economics and the theory of comparative advantage of David Ricardo.

What is the difference between positive theory and normative theory?

“Positive theory is a theory that tries to explain how the world works in a value-free way, while a normative theory provides a value-based view about what the world ought to be like or how it should to work.

Can positive theories assist normative theories?

Positive theory has expanded accounting theory from the purely decision making focus of normative theorists into analysis of political and economic factors.

What are the assumptions of positive accounting theory?

Under Positive Accounting Theory, the assumption is that a manager will exhibit opportunistic behaviour and choose accounting policies that are in her/his best interests.

Why is positive accounting theory important?

Watts and Zimmerman's Positive Accounting Theory provides a refreshing, controversial and important contribution to accounting thought. It is important because of its vigorous emphasis on the entity's actual choice of financial accounting technique (or, more broadly, financial reporting activity).

Who created positive accounting theory?

Positive Accounting Theory (PAT) that popularized by Watts and Zimmerman is one of positive theory accounting. PAT is concerned with explaining accounting practices. It is designed to explain and predict which firms will not use a particular method.

Who propounded positive accounting theory?

Positive accounting emerged with empirical studies that proliferated in accounting in the late 1960s. It was organized as an academic school of thought of discipline by the work of Ross Watts and Jerold Zimmerman (in 1978 and 1986) at the William E.

What is the difference between normative and positive accounting?

Whereas, normative accounting theories, utilised a model which is completely different from the positive theories of accounting. As per normative theory of accounting, the analysts would give an accounting approach to be pursued in this scenario based on the incidents that have took place. The positive accounting theory will significantly influence the company's response at moments when a unique accounting norm is implemented on the economy. The positive accounting principle can help illuminate the company's accounting practices.

Why use normative accounting principles?

At the same time, the normative accounting principles could be used to offer guidance on existing policies that can be included in the same manner to diverge or strengthen it . The methodology to normative accounting principles that has been pursued is distinct from the positive theory of accounting.

What is normative theory?

The normative theory of accounting offers the needed guidelines that can be used to make the accounting policy segment suitable for management. Simultaneously, the normative accounting principles can also be used to give guidance on existing regulations that could be utilised in the same manner to strengthen it.

What are the three hypotheses developed under the positive accounting theory?

The 3 key hypotheses developed underneath the positive accounting theory by Watts and Zimmerman (1978) are: the hypothesis of the bonus plan, debt/equity, and the hypothesis of political cost. Taking a look at the fundamental analysis for this hypothesis, it is obvious that all of these hypotheses are focused on self-interest.

What is positive accounting?

The positive accounting principle can help illuminate the company's accounting practices. Introduction: The positive theory of accounting offers an insight of the bookkeepers' illustrative behaviour. Whereas, in positive theory of accounting, the firm's administration tends to use the strategy of adopting accounting laws and norms ...

Why do administrators transfer present financial year's income in coming years?

Therefore, there may be a risk in these situations that the administrators will follow an accounting principle that will transfer the present financial year's income in coming years to save the forecasted political price. High income can also result in high taxation and often high restrictions. (Watts, 1990)

What is debt covenant hypothesis?

Debt covenant hypothesis: Businesses that are added probability of breaching the debt agreement are supposed to choose the bookkeeping rules that enable auditors to switch to the current cycle the financial return that the organization is projected to recognize.

What is normative accounting?

Normative accounting. Normative accounting, most commonly found in a company’s business or marketing plan, takes a subjective approach. Based on abstract principles, it endeavours to characterise what the financial future of a firm should look like.

Is normative accounting a form of accounting?

While a firm may choose one form of accounting over another , it is more common that businesses in general use a combination of both positive and normative accounting. Looking at the bigger picture of accountancy practice as a whole, financial experts create new standardised policies using normative accountancy theory, however these policies are based on the factual justifications found in positive accounting. The objective nature of positive accounting creates the foundation for enterprises to employ normative accountancy theory within their business.

What is positive accounting theory?

Positive accounting theory, known as the ‘practical approach ’, looks at what is currently happening in a business; it’s based on cold, hard statistics. This approach is regularly used within bookkeeping and data collection; positive accounting scrutinises the real world transactions of a company and compares the incomings with the outgoings to identify any discrepancies. This approach allows the accountant to see whether a business is making or losing money. The theory provides accountants with a framework from which to predict how the company will account for transactions going forwards. Here is an example of a positive accounting scenario from Pocket Sense – a company that helps individuals manage their personal finances: “if corporate growth allows a company to increase shareholder dividends over previous dividend payments, positive accounting theory would conclude that corporate growth causes a rise in stockholder dividends.”

What is normative accounting?

Unlike positive accounting which is based on observation, normative accounting theory advises policy makers on what should be done based on a theoretical principle; it starts with a theory and deduces specific policies from this. While positive accounting looks at past data, normative works with events in the future.

What are the two theories of accounting?

Today we will be discussing two theories which are commonly used – positive accounting (a practical approach) and normative accounting (a theoretical approach) – and looking at which of the two delivers the best overall picture ...

Is practical accounting normative?

Both practical and normative accounting are influential theories, but which of the two is preferred and can or should they be used together? Today, although a business may opt for one theory over the other, it’s common place for a company to use a combination of practical and normative; in many cases, the theories complement each other. Those within finance may use normative accounting theory to come up with new policies, but these standardised policies are usually based on the factual explanations identified in positive accounting.

What is positive accounting?

Positive accounting. In positive accounting theory, academics view a company as the total of the contracts they have entered into. The theory posits that, because companies are fundamentally about the contracts that dictate its business, a core driver of company success is efficiency. That means minimizing the costs of its contracts to unlock ...

Why were banks accounting for financial securities?

The banks were accounting for financial securities in a way that hid material changes in their value that was pertinent to the bank's operation. That change in value was germane to the financials of the companies, and the day-to-day practices were no longer presenting an accurate representation of the company's financial position.

Is positive accounting more theoretical than normative accounting?

Positive accounting is very practical, and based on what's actually happening. Normative is more theoretical, ensuring that, as day-to-day practices evolve, they don't diverge from appropriate economic concepts.

Is accounting arbitrary?

All of the different accounting rules are not arbitrary or naturally occurring, though. Today's accounting systems are the result of carefully constructed applications of theories that seek to find the best and most economically accurate methods for representing a company's performance. Two of those theories are positive accounting ...

Is normative accounting more deductive?

Logically, normative is more of a deductive process than positive accounting theory. Normative starts with the theory and deduces to specific policies, while positive starts with specific policies, and generalizes to the higher-level principles.